Introduction

One of the benefits of having BIO in Boston is that it provides me with a ~3.5 hour drive back to New York. This gives me a chance to mull things over while playing Spanish rock music at 11 (like 10, only louder).

This year’s drive back was no different. But this time, there was a lot to mull over, especially at a macro level. The global financing and political environments, which really started to turn against us in January, have really placed our industry in a rather difficult position (or, perhaps positions is the proper word here).

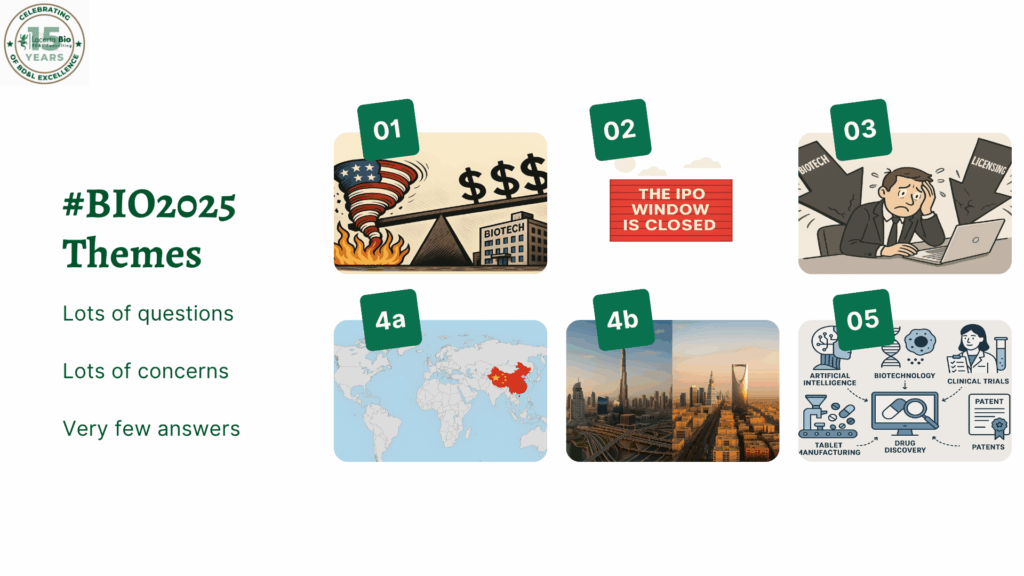

The drive resulted in five themes which emerged from BIO. These themes come from conversations I had with folks in Partnering, plus conversations with friends and colleagues I met informally during the week…all supplemented with some additional research over the weekend.

As we approach the mid-point of 2025, it is impossible to plan for or to predict what will happen during the rest of 2025 and beyond.

And this is the crux of the problem.

Every day it seems as if we are facing a new challenge or crisis that works against our industry. Case in point: as I am writing this, the news of American bombs dropping in Iran is making the rounds, which does not help matters.

These five themes are by no means conclusive nor complete. I tried to limit myself to 3-4 paragraphs per theme, just to keep things short and digestible. In some cases, I completely ignore some social and related issues, again for the purpose of keeping things short and focused.

Theme #1: US Political Volatility and Its Growing Cost to Biotech

The mood at BIO 2025 was clear: the US political climate is no longer just a nuisance — it is becoming a strategic and financial risk for our industry.

Several attendees voiced concerns over deteriorating federal support, escalating supply chain-related costs, and the chaos around regulatory and immigration policies (which can change at any moment).

Some individuals I spoke with discussed the possibility of reducing US presence or relocating company operations entirely to tap into other sources of capital and to enjoy more stable political environments.

Similarly, there were also efforts mentioned to recruit academic scientists from the US to more stable environments, such as the UK, EU, or even the Middle East (more later).

The implications for grant funding were particularly striking. Recent reports suggest the US government is terminating federal grants to biotech firms and academic labs with connections to certain countries (and not just China). Concerns over this were expressed by a few of the people I met.

Policy meddling was also a recurring theme. From the political interference in the ACIP vaccine agenda to delays at the FDA affecting cell and gene therapy reviews, companies are bracing for milestone disruptions, product launch delays, and regulatory unpredictability.

Add to that the proposed legislation to ban direct-to-consumer (DTC) advertising of pharmaceuticals, and the result is growing anxiety among US biotechs and their investors.

This may sound somewhat alarmist, but I am beginning to think that the US risks squandering its long-held leadership in biotech innovation. As legal, financial, and regulatory headwinds mount, startups and scale-ups are increasingly eyeing jurisdictions that offer not just capital but also political and economic stability.

If current trends continue, the next wave of scientific breakthroughs may originate outside the US ; not because the science is better abroad, but because the system here makes it too hard to stay.

Theme #2: The Biotech Liquidity Bottleneck

Everyone I spoke with agreed on one major industry-wide problem: the continued (and relative) closure of the biotech IPO window.

For venture-backed biotech companies, this means no clean exit path for their investors. Without IPOs, gains cannot be realized, and the flywheel of innovation stalls. Capital that is tied up in private companies cannot be recycled into new funds, and then startups. LPs are discouraged from investing in new funds, instead investing in funds investing in other industries. While there were ~30 biotech IPOs in 2024, and 10 so far in 2025, it is still not a great pace compared to prior years.

Several of the service providers I met (CROs, CDMOs, and consultancies alike) have baked in “zero growth” scenarios for 2025, anticipating that the sector will tread water while waiting for the capital cycle to reset (assuming they can survive until then).

That wait has already gone on too long for some. According to EY, more than one-third of biotech companies have less than 12 months of cash remaining — a cash cliff exacerbated by macroeconomic pressures, looming patent cliffs, and lingering regulatory and policy uncertainty, as discussed previously.

Platform companies are now being judged almost entirely on their lead asset, forcing teams to abandon broader pipelines in a bid to survive. This pressure is resulting in budget cuts (mainly personnel) to focus cash on the lead candidate. But this also means that a huge volume of science is being left undeveloped, perhaps ready to be plucked by savvy investors at rock-bottom valuations.

Speaking of which, private equity investors are actively exploring the purchase of VC-held shares in biotech via a range of new and existing vehicles. Companies like Revelation Partners and Blackstone Strategic Partners are enabling early VC backers to partially exit and return capital to LPs.

This activity doesn’t solve the IPO problem, but it helps address the liquidity crunch and may offer VCs some breathing room until they (try to) raise their next fund.

Companies like Syncona are pivoting to meet this reality head-on. The publicly listed UK-based investment firm recently acknowledged a “challenging market” and is doubling down on later-stage biotech companies, potentially preparing to raise a new fund.

But Syncona’s investments in some of the riskiest areas in our industry (such as CAR-T and gene therapy) may make these pivots challenging, especially as Big Pharma continues to reduce their licensing activities in these modalities. Can we see future investments shift away from cell and gene therapy and towards less risky modalities? Possibly.

Could SPACs stage a comeback? Possibly. Veraxa’s recent SPAC is quite interesting. In fact, I had one ex-US client ask about SPACs to raise capital in the US. This not an area of my expertise, and I have not followed trends in SPACs closely at all. But apparently, there have been 58 SPAC IPOs so far this year, across multiple industries. How many of these are healthcare-related is unknown. I suppose for the right company with the right portfolio, it may be possible. But the underlying fundamentals discussed previously will likely make this approach challenging.

To be clear, capital is being invested in biotech. Projections suggest we will see venture investments in the $25-30 Billion range this year, roughly matching historical norms. But the number of rounds will be flat to reduced. In other words, the trend will continue of seeing more capital being invested in fewer companies. To quote from Nature Biotech (with my emphasis):

Biotechs with good clinical data and those with assets in fashionable fields like neurology, cardiometabolic diseases, immuno-inflammation or popular corners of cancer (such as multispecific antibodies or antibody–drug conjugate (ADC) technologies) are attracting a disproportionate share of VC dollars. That’s because these assets are most likely to be selected to fill valuable slots in Big Pharma pipelines. Many of the rest — platform-based, preclinical or just data-silent biotechs, private or public — are languishing.

When will the bottleneck open? Will we ever see the frothy markets we saw in 2020 and 2021? For the latter question, the question is a resounding YES. But when? We went ~20 years in between bubbles. So I don’t think the froth will return anytime soon (especially with this geopolitical and geoeconomic environment). But struggling companies may have plentiful candidates that have excellent potential in the hands of the right buyers.

To paraphrase Warren Buffet, there is fear in the current markets. Is now the time to be greedy and buy?

Theme #3: Licensing Environment

It’s a tough environment right now if you are a prospective Licensor. There is no getting around it. Every Licensor I met with at BIO made similar statements about the challenges of securing meetings, let alone moving into post-CDA discussions. And while poor out-licensing process can be at the heart of it, it is clear that the narrowing focus by Licensees is driving these challenges.

At BIO, one of the clearest themes was a growing perception that Big Pharma is becoming more risk-averse, demanding later-stage data—particularly clinical proof-of-concept (POC)—before signing licensing deals.

But is this true?

Historically, a significant proportion of deals—30% to 50%—have involved preclinical assets, and there’s little hard data to suggest that number has collapsed (and if someone has licensing data by stage of development for the First Half of 2025, please let me know). However, in today’s tighter capital environment, it’s fair to question whether that proportion will hold in 2025.

A major driver behind this disconnect is the 2020–2021 financing boom. Flush with investor capital, many companies moved candidates and platforms forward aggressively. Now, with that capital largely spent, these same companies are trying to secure partnerships based on the data they’ve generated.

Many of those programs are failing to resonate with potential licensees. It’s not necessarily because the data are weak – some of these candidates are quite promising, But rather because the commercial theses underpinning them were (or are) flawed.

Licensees, particularly Big Pharma, are constantly thinking about the evolution of standards of care and commercial markets (especially reimbursement). Candidates with great clinical data but an underwhelming commercial rationale will struggle to find a home. Companies with these kinds of candidates may have to raise enough capital to commercialize it themselves, a task that is increasingly difficult in the US, as discussed above (more on this point later).

This environment has left a swath of biotechs stranded: unable to raise new funds, unable to secure licensing deals, and facing dwindling cash runways while answering to impatient GPs (who are facing their own pressures from their investors).

The result is a growing inventory of clinically advanced, potentially valuable programs available at steep discounts.

Will we see more acquisitions of stalled programs – either through direct asset purchases or secondary vehicles that recapitalize and refocus these assets? It’s an interesting question. In other words, the licensing bottleneck could actually be a buying opportunity in disguise for those with capital and conviction.

For forward-looking investors and new fund strategies, I believe they have a window of opportunity. Asset-rich, cash-poor companies are plentiful. If a fund is willing to step in, acquire promising but stranded assets, and carry them through late-stage trials and into commercialization – especially in the U.S. – the potential returns could be substantial.

Those who can do it might find themselves building the next generation of specialty pharma companies from the broken pieces of the post-COVID boom.

But this isn’t a quick-flip strategy. It requires operational expertise, long timelines, and a willingness to assume the possibility that a US or Global Licensee will not present itself until the product is commercialized in the US or other major market. How many investors (especially those outside of biotech) fit this description?

For Big Pharma Licensees/Acquirors, it remains a buyer’s market. With over 20,000 candidates in active development (but with more than half in Preclinical), there is no shortage of opportunity.

We will likely continue to see a few, large, headline-grabbing transactions for relatively mature candidates in very selective therapeutic areas and indications. But I believe the number of licensing transactions in 2025 will be reduced relative to prior years; we’ll just have to wait and see if this turns out to be (unfortunately) correct.

Theme #4a: China

One of the most noticeable shifts in our industry is the pace at which innovation is emerging from China, especially over the past two years. China is now generating competitive therapeutic candidates that are being licensed outward—notably westward. In many ways, China is displacing Japan as the principal source of Asian innovation.

This trend was a recurring theme at BIO 2025, where numerous attendees noted how Western companies are now seriously evaluating (and licensing) China-origin assets, particularly in oncology, autoimmune disease, and cell therapies. According to recent data, Chinese biopharma companies executed 48 outbound licensing deals in 2023 alone, up from just 15 five years ago .

However, the political climate in the U.S. casts a shadow over the viability of some of these deals. Restrictions on Chinese investment and growing scrutiny of cross-border IP and data flows make it increasingly complex for U.S.-based companies to engage in licensing transactions with Chinese firms (cf., Theme 1).

Such deals may be deemed politically sensitive or trigger CFIUS review. This may be creating an atmosphere of hesitation among U.S.-based licensees, especially in the current US political environment.

Some firms may consider in-licensing Chinese assets for non-U.S. territories, such as Europe or Latin Americ., but the economics of those regions may make it hard to justify. Pricing controls, slower regulatory timelines, and payer fragmentation (especially in the EU) make it challenging to build viable, sustainable business cases. This makes what some of the MENA countries are doing quite interesting (more later).

The fundamental issue is that the U.S. remains the only truly scalable, premium-priced pharmaceutical market. Building a base case financial model without assuming eventual U.S. approval and reimbursement is extremely difficult.

For Chinese-origin assets, this means their global potential is materially discounted if a path to the U.S. market is uncertain. Nonetheless, there are signs that some European companies are willing to take that risk, especially if they can obtain regional rights at a meaningful discount.

Moreover, Chinese companies are also starting to adapt: designing global trials, hiring U.S.-based executives, and forming strategic partnerships to mitigate perceived regulatory and geopolitical risks.

As discussed in an article in Forbes recently (if you can get past the pop ups and the videos), the Chinese government enacted policy reforms to make local clinical studies and approvals much faster. This means that candidate emerging from China may be not only innovative, but backed by a substantial amount of Preclinical and Clinical data.

In parallel, China’s domestic markets are maturing rapidly. IPO activity in Shanghai and Hong Kong has picked up again after a temporary slowdown, with biotech companies increasingly tapping these markets for capital. This means Chinese innovators are under less pressure to sell cheaply or early – they have options.

Other countries in the region, especially South Korea and Taiwan are following suit by leveraging their capabilities to expand their local biopharma industries, especially in biomanufacturing.

My friend Tosh Nagate had an interesting idea. What if you established a common, harmonized pharmaceutical industry between Japan, Taiwan, and South Korea? This EU-like model would leverage the strengths of each country into a common market. Those three countries have a combined population of ~200 million, compared to the population of the “Big Four” EU countries of ~250 million. Imaging signing one out-license that covered all three countries simultaneously, with an attractive pricing and reimbursement model (and local manufacturing). That could be interesting.

Notwithstanding, for Western companies and investors, this dynamic presents a strategic dilemma: ignore China and miss out on an emerging innovation superpower, or engage with caution and develop new frameworks for navigating its complex commercial and regulatory landscape (while simultaneously considering a business case that excludes the US).

Theme #4b: The Middle East

While passing through the Exhibition, I bumped into my friend Tushar Nuwal right outside the Saudi Arabia booth. He suggested that we grab a cup of Arabic coffee in the booth because the coffee is “amazing.”

He was right. That was a great coffee. It was light, spicy, and very tasty. I know nothing about Arabic coffee. This may have been the Tasters Choice of Arabic coffee. But it was darn good.

But why were they at BIO in the first place? Rest assured, they were not there to introduce naïve attendees like me to their coffee.

As I learned from my chats with the folks in the Exhibition, The Middle East is emerging as a strategic region for biotechnology investment and innovation, with Saudi Arabia and the United Arab Emirates (UAE) leading the charge to diversify away from the petroleum industry into other, more innovative sectors like biotech.

Their approaches are multi-pronged: building cutting-edge infrastructure (such as laboratories and manufacturing facilities), developing regulatory environments for commercialization across the entire MENA region, fostering public-private partnerships, and investing in talent attraction and retention.

What really strikes me is their long-term perspective and highly ambitious approach. They are not looking to innovate themselves into success (like China). Instead, they (and by “they” I mean both national governments and private investors) are building the infrastructures (physical, human, and financial) that will, over time, lead to innovation and value creation.

Post-BIO, I had a chance to look into this further, and I am amazed at the scale of these efforts.

For example, Saudi Arabia’s National Biotechnology Strategy, launched in 2024, lays out a roadmap to become the biotech leader in the MENA region by 2030 and a global hub by 2040, focusing on vaccines, genomics, plant science, and local biomanufacturing capacity. Note that the goal is only 15 years away, which is not long in our industry.

Partnerships like the one with Vertex Pharmaceuticals to localize gene therapy manufacturing reinforce the government’s commitment to fostering a biotech ecosystem with global linkages.

The UAE, too, has made biotechnology a central pillar of its economic diversification agenda. Abu Dhabi and Dubai are investing heavily in genomics, digital health, and agricultural biotech, with initiatives such as the Emirati Genome Programme projecting tens of thousands of new jobs by 2045.

The government is fostering a startup-friendly environment through dedicated incubators, financial incentives, and access to capital. Infrastructure developments like the very impressive Biotechnology Research Center(BRC) reinforce the UAE’s goal of becoming a regional hub for both biotech R&D and commercialization.

It is clear that countries in the Middle East are investing heavily to become participants in biotechnology innovation, and not merely as a commercial afterthought for approved products.

Innovation…infrastructure…capital…these are no longer the exclusive purview of the US and Europe. Our industry is quickly shifting Eastward.

It may only be a matter of time before a NewCo is formed in an incubator in the Middle East, led by Managers and Scientists from the US and EU/UK, working on candidates licensed from China, funded by Middle Eastern sovereign wealth funds, and developed and commercialized globally outside the US…creating value while avoiding the anti-industry whims and challenges being presented by the current US Administration.

Theme #5: Artificial Intelligence

At BIO, I had the good fortune to catch up with Joseph Beck of NeuroSolis. During a wide-ranging discussion, we briefly talked about preclinical models for the development of candidates to treat pain, and he told me about the Grimace Model.

“What is the Grimace Model?” I asked.

Apparently (and this was all news to me), researchers visually and manually score facial expressions in mice and other animal models to assess pain levels—a technique known as the Grimace Scale.

My response? “Seems like the perfect opportunity for an image-based analysis using AI.”

I am not an expert in AI, but it seems to me that training an AI model on thousands of annotated images could create a gold-standard, scalable method for pain scoring, reducing inter-rater variability and accelerating analgesic discovery.

The fact that this was an obvious idea to me (a non-expert) leads me to conclude that AI is simply everywhere in our industry consciousness. In fact, very few discussions at BIO did not touch on AI in some way.

AI is now embedded in everything from compound design and screening to clinical trial design, patient identification, manufacturing optimization, and IP strategy.

At the heart of AI’s appeal is its ability to ingest, interpret, and learn from complex, heterogeneous datasets—spanning genomic sequences, EMR records, imaging data, and even handwritten lab notebooks—with a speed and scale humans can’t match.

Beyond research, AI is now making inroads into previously “high touch” domains like patent writing and IP strategy. At BIO, several conversations touched on emerging platforms that can draft provisional patents or assist in identifying gaps in existing IP claims.

One example is Lightbringer, a startup developing tools to automate patent drafting. The promise here is not just speed or cost savings—it’s about enhancing the quality of IP strategy by surfacing unexpected overlaps or omissions. For early stage biotechs with limited legal budgets, this could be transformative (and law students may want to have a career rethink…). Overall, the sense at BIO 2025 was that we’ve passed the AI tipping point. AI is no longer a specialized tool wielded by computational scientists. It’s becoming a general-purpose enabler for every aspect of biotech innovation. From preclinical discovery to regulatory strategy, from animal models to investor decks, if there’s a task involving information, there’s probably a model for that—or soon will be.

#BIO2025 Themes: Conclusions

I tried to come up with one word to summarize the sentiment as I perceived it at BIO2025. The word disquietcame to mine. I thought anxiety and stress, while perhaps applicable to some attendees, were a bit too strong to describe the mood (or, vibe if you are under 30).

Why?

This was the first BIO after the new US Administration came into power in January. In a mere 5 months, it is safe to say that the already difficult environment has become even more difficult.

Statements, policies and actions undertaken from the current administration are largely working counter to our industry’s objectives (including academia)….Not only making our lives challenging, but potentially discouraging investors from our industry in the search for other higher-risk/higher reward investment opportunities without the political baggage.

Meanwhile, other countries are stepping into this emerging vacuum, investing in innovation, infrastructure, and talent attraction.

Even our closest allies, such as the United Kingdom, are executing on ambitious plans to grow their domestic biopharma industry.

These are governments who view our industry as a source of economic growth and economic diversification, and they are investing accordingly.

Separately, the liquidity bottleneck lacks a clear solution. The US Federal government is limited in what it can do, aside from tax cuts, reduced regulations, and so on. And these things take time.

Ultimately, it is up to the markets to correct themselves. But this takes time, which is something a lot of companies and patients do not have.

There are (probably) a number of really good candidates which are just sitting there, with patent clocks ticking, ready to be resuscitated via a splash of capital and development expertise.

Drug development continues to be largely a Buyer’s market, but new models (SPACs? Divestitures & Spin Outs?) and new geographical considerations (move to Dubai?) means that Sellers must be increasingly flexible and creative in how they advance these candidates beyond traditional approaches…especially in an increasingly challenging licensing environment.

So, in my view, much of the disquietude is from a sense that we (Our country? Our industry?) are simply not going in the right direction, while simultaneously powerless to do anything about it.

What happens now?

I have no idea.

Meanwhile, AI and other innovations are demonstrating that our country and industry possess resilience, creativity and optimism…qualities that are difficult to replicate elsewhere in the world.

Besides, this is the biopharma industry. There are many examples of, for example, listed companies who traded below cash value, only to restructure and resurrect themselves.

So, the best we can do is to carry on.

I will keep these themes in mind during the rest of the year and revisit them once again in our annual Year in Review Video, which will be released in December.

Sincerest thanks to everyone I met with, which is a list too long for this article, and who unwittingly contributed to these Themes during a very interesting week in Boston.

I also would like to thank CHArles T. GePokenTosser for his tireless research efforts and comments on my early drafts.

FAQs

- You did not discuss the efforts taking place in Country __________

This is correct. There are many other countries doing interesting things to grow and develop their own domestic biopharmaceutical industries. This is nothing new. But when countries are investing and the US is seemingly moving backwards, it makes one wonder if some of these other countries will be increasingly successful in the years to come.

- You did not discuss the social and political issues of Country _______

This is also correct. Some of the countries mentioned (and I will include the US and its current stance on immigration / deportation) have domestic issues and policies which, to some people, violate basic human rights. But I wanted to stick to issues surrounding our industry, as I am in a poor position to comment on these and other issues.

- Do you think I will lose my job as a ______ to AI?

If the agentic AI being deployed in your department is cheaper and as good (or better) than you are, then you will lose your job. How are your barista skills?

- Do you actually think countries in the Middle East will become new biotech hubs?

I have no idea. But these and other governments in the region are looking at biopharma as one of several industries of focus when it comes to economic growth and diversification.

The key point, in my opinion, is that they are investing massively into infrastructure and talent attraction. From their perspective, the original innovations can come from anywhere, not necessarily a local university. They are not limiting themselves to whatever their local universities are doing (although those are being enhanced as well).

This is a huge difference compared to what many other governments are doing. Can you imagine the US or UK government building a biotech incubator, for example?

Me neither.

- When will things return to normal?

Never. Time moves forward, never backwards. To quote Pessoa, “To be normal is the ideal of those who have no imagination.”

- You are completely wrong when it comes to _______

Entirely possible. Nothing is certain. Our industry provides many things (treatments, cures, extended life, employment, taxes, etc.), but certainty is not one of them. Again, Pessoa, “The act of thinking turns the absolute into uncertainty.”