Finding myself with a lengthy layover at the Dublin Airport in Swords, Ireland, on my way to New York from BIO-Europe (and with a surprising lack of Guinness at the airport…in Dublin of all places), I decided to document my impressions of the “vibes” from the conference in Vienna.

Conference vibes are always difficult to characterize because conferences like BIO-Europe tend to be a lot of fun. We interact with industry colleagues in very social, positive settings (especially those when the beverages are free-flowing).

Everyone is happy to be out of the office for a few days, especially in a beautiful city like Vienna. Politics…wars…for many attendees these issues are forgotten for a few days. What reason can there possibly be to be unhappy in such a setting?

And yet, if we wipe the steam off the window pane, we can see (and hear) several items of concern. Some of these repeat the themes we discussed in our post-BIO series of articles. Thus, in no particular order…

Where is the venture?

Many companies, including some of our own clients with very interesting data and well-defined commercial stories, are struggling mightily to raise venture financing.

Numerous posts on LinkedIn also suggest that we are experiencing a financing winter, with even the smallest of financings being hailed as a “green shoot” that will trigger a return to the good old days.

Others have suggested that pending patent expirations of blockbusters will trigger a loosening of the purse strings and a wave of both M&A and licensing.

But I don’t buy this argument for a moment. It is not as if a Big Pharma CEO woke up one morning and said, “Hey! Our blockbuster is about to expire in a few years. We should do something about this.” Regardless, we will leave this idea here for purposes of the discussion.

Is any of this gloom and doom real? Is it clickbait? Or something in between?

Before delving into the details, we should keep in mind that financing data are are imperfect, irrespective of the source. A small investment by Rich Uncle Pennybags in an FFF round is unlikely to trigger the public statement necessary for inclusion in these datasets.

Some datasets exclude transactions below a certain threshold, even when publicly disclosed. Further, the press releases rarely release enough financial and structural details in their description of a particular transaction. Thus, any of these data should be interpreted as directionally correct, but not 100% accurate.

Given these caveats, let’s look at the data.

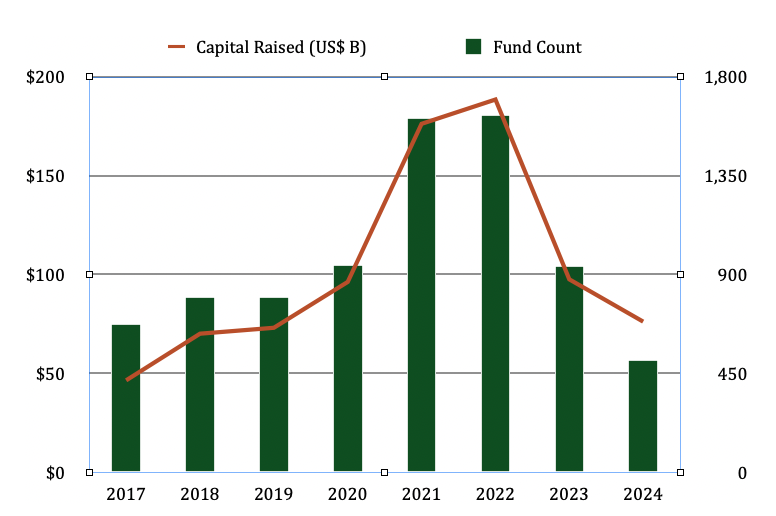

The Big Picture: Venture Capital Fundraising 2017–2025

The US venture capital industry has experienced a dramatic cycle over the past eight years, from a modest baseline in 2017-2019, to the boom of 2020-2022, and then to what some call a “reset” in 2023-2024. After the reset, where are we relative to the pre-pandemic era?

The entire US VC industry raised an average of ~$63 billion per year across the 2017-2019 period. Entering the pandemic era, we experienced a sharp increase in fundraising, peaking at ~$189 billion in 2022.

This peak was influenced by low interest rates, plentiful liquidity, and tourist investors looking to cash in on the venture capital boom. In 2023 the industry retrenched, with commitments dropping to approximately $100 billion, then $76 billion in 2024 (orange line in graph above).

Thus, we have definitely experienced a sharp decline in VC fundraising from LPs since the 2021-2022 bubble. But as of 2024, we remain at or above historical averages.

How much was raised during the First Half of 2025 by VC funds in the US? That’s the question, and it is a difficult one to answer.

According to Reuters, only ~$27 billion were raised by 238 venture capital funds in the US in the First Half of 2025. Assuming for a moment that 2025 ends at ~$60 billion, the industry will return to levels at or below those the 2018-2019 pre-pandemic era.

Median time to close (15.3 months) was also longer, perhaps reflecting a loss of confidence in the venture capital model relative to other investment opportunities available to limited partnerships.

In addition, roughly 75% of VC fund commitments in the U.S. went to just 30 firms in 2024. Indeed, new venture funds peaked at 441 in 2021, dropping to 103 in 2024, reflecting the challenges faced by new fund managers to convince reticent LPs to invest with them versus other GPs.

Thus, it is safe to say that the entire US VC industry has experienced a boom cycle. Is in a bust cycle at the moment? The trend appears to be indicating this. We will have to see where the figures for 2025 land.

It may be a bit much to say that the venture industry is “collapsing” as some have said. Perhaps “concentrating” and “retrenching” are better descriptors.

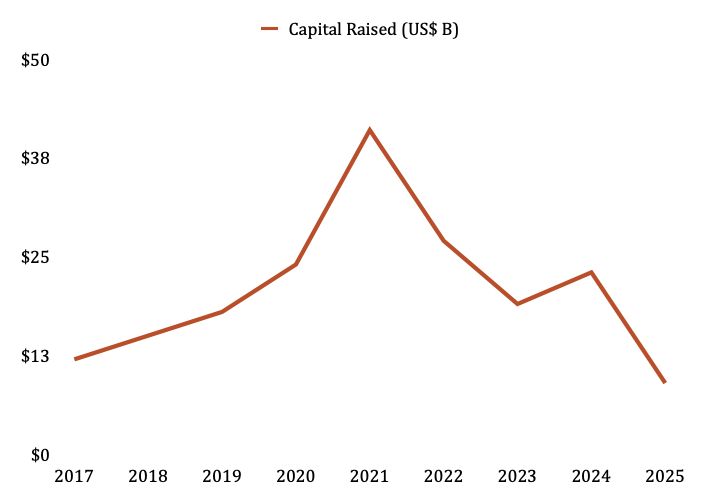

Focus on Healthcare Venture Capital

Silicon Valley Bank has tracked healthcare venture capital fund flows for years. Reviewing their Mid-Year 2025 report, they describe the current fundraising environment as being in a “free fall.”

From the $41 billion peak in 2021, SVB estimates that 2025 will end with a mere $9 billion in capital raised by healthcare VCs, a level not seen since 2016.

Uncertainties triggered by the policies and pronouncements coming out of Washington DC (tariffs, reductions in grant funding, etc.) has triggered a number of secondary effects, such as a sharp rise in international applications by US scientists to research positions outside the US. These and other factors are shedding a negative light on our industry relative to others from an investment perspective.

Companies who leverage AI in some way are receiving a disproportionate share of the smaller amount of capital available. Therapeutic areas of VC interest (and, by extension, of Big Pharma / Licensee interest) include cardio-metabolism (mainly obesity and related conditions), neurology, autoimmune diseases, and of course, oncology. This comes at the expense of nearly everything else.

An extremely weak IPO market has not helped matters. From 81 and 96 healthcare IPOs in 2020 and 2021, we saw a mere 23 IPOs in 2024, and only 9 in the first half of 2025.

Implications

This is a problem, to put it mildly.

Companies who would have been financed a few years ago are simply no longer competitive in a market where the supply of capital is falling sharply. GPs who tell CEOs to “do more with less” are finding themselves heeding their own advice.

When will the capital markets return to historical levels?

If by “historical” we mean 2020-2021, then the answer is likely “never.” The perfect storm of a global pandemic, low interest rates, and frothy public markets are unlikely to return in our lifetimes (cf., the 2000 “omics” boom).

Many companies who raised capital during the boom have spent that capital; some successfully, some not. For some of those companies who have spent it well (that is, by generating new, interesting data), they might be able to raise additional, larger rounds this time around, likely from established VCs who, in turn, have recently closed on new Funds.

This will likely be a rare event relative to the number of companies who cannot raise follow on rounds, either due to marginally impressive data, data on a candidate(s) with a poor commercial hypothesis, or companies who simply cannot compete for the attention of VCs with available funds…many of whom are reserving dry powder to support companies already in their portfolios.

This is further complicated by the fact that LPs always have alternatives, many of which simply have much lower risk and a marginally lower reward. We have industries (like AI) which can deliver outstanding returns much faster, with lower risk. Why invest in cell and gene therapy when you can invest in AI-powered insect and plant identification apps?

However, as Warren Buffet has pointed out by paraphrasing the old Rothschild adage, this may be a “blood in the streets” moment for our industry.

Just because a company cannot raise capital does not mean that the company has an inferior candidate(s). Maybe the Management Team cannot communicate well. Maybe they simply do not know what they are doing from a marketing and messaging perspective.

Who knows.

But savvy investors and entrepreneurs may be able to look past the CEO-speak and find some really interesting candidates that need capital and a fresh development and commercial plan. We’re not taking about another GLP-1 here. Rather, these will be novel candidates hitting novel targets which need a bit of investment to finish IND studies, to generate new data in additional animal models, or to clarify some CMC issues. These could also be candidates that can be repositioned in another indication.

Thus, due to the financing environment being what it is, we anticipate the number of earlier-stage candidates available for licensing will increase because their investors will want the exits to support their fund raising. This may create an unprecedented buying / investment opportunity for those with the resources and smarts to identify promising candidates and negotiate highly favorable terms.

AI: Friend or Foe?

Billions of electrons have been spent writing about the impact Artificial Intelligence will have on our industry, especially when it comes to drug development. This is generally viewed as a positive and massive step forward, especially if AI can be used to discover novel candidates faster and simultaneously reduce clinical development expenses, all while reducing development risk and increasing Probability of Success.

However, the machines will learn how to do our jobs, and will do them much faster and cheaper than we can. Jobs will undoubtably be lost, especially in positions where any sort of evaluation or analysis is required (i.e., financial modeling, due diligence, etc.).

The recent news that OpenAI is hiring experienced investment bankers to train its AI to build financial models, plus the efforts of investment banks to create their own AI-based financial modeling modules, means that these tools will eventually make their way into other industries, including ours.

Beyond financial modeling, it is easy to envision a day when large, complex diligence efforts are mainly performed by AI, simply because AI is not only faster, but better at consuming, digesting, and summarizing large, disparate sets of information, such as what is found in a data room.

Don’t believe me?

Ok.

Then check out platforms such as Gosset, Bioneex, and Partex.

AI is not the future. It is here already.

Beyond the BD&L team, nearly anyone across the value chain who performs a routine task will be vulnerable to replacement by AI.

Is this making you nervous? You should be.

Those who take the initiative to “up-skill” will likely benefit at the expense of those who do not. The question, of course, is how many of our current roles fall into the category of “routine.”

According to Dr. Andree Bates, a leading expert on artificial intelligence in our industry,

AI can potentially replace up to 25% of drug discovery jobs by expediting target identification and compound screening processes. In clinical research, up to 21% of roles, such as patient recruitment coordinators and trial inspectors, could be automated. Commercially, AI may substitute for up to 14% of sales and marketing positions by driving hyper-personalized engagement.

Reskilling in the AI Era for Pharma Professionals, Dr. ANdree Bates

McKinsey reports that generative AI can produce over $110 billion in annual value (whatever “value” means) across our industry value chain, both by reducing costs and accelerating or improving innovation.

Now I have no idea where these numbers come from. It is probably too early to accurately quantify the impact of AI in terms of OpEx savings, diligence speed, and other metrics.

Interestingly, at BIO-Europe, there was some denial of the potential for AI to replace jobs.

But the reality is that any technology which can accelerate a process while reducing its cost will be deployed, at the expense of an employee or two.

It has always been this way, and it will continue to be.

China

The aforementioned SVB Mid-Year Report has a very interesting slide loaded with data on China. To summarize:

- Both the number of licenses and the value of these licenses from Chinese companies are growing rapidly.

- Chinese innovators are excelling at discovering novel antibodies, with antibody-specific deals growing in terms of Upfront Cash and Equity.

- Candidates emerging from Chinese companies are backed by more data, especially more clinical data, thanks in part to their ability to generate clinical data cheaper and faster than comparable companies in the US and Europe

- A direct license to a Big Pharma company is not the only model. NewCo formation licenses to small and mid-cap companies are also being executed.

A panel discussion at BIO Europe emphasized a few of these points. Many candidates coming out of China are more innovative and backed by more data versus comparable candidates coming out of the US or Europe.

However, a Chinese company cannot rely exclusively on the Chinese market for commercialization. Chinese innovators must out-license ex-China rights to achieve acceptable ROI.

So the flow of candidates, many of which were initially financed during the boom, will continue in the near-term. Indeed, this flurry of outbound licensing from China coincides with capital scarcity in the West, creating a striking asymmetry of supply and demand for innovation.

This has profound implications for Western companies seeking Licensees.

It has simply become far more competitive in terms of securing a lucrative license because many of these candidates emerging from China are very competitive, if not better, than anything being generated in the US or EU, especially when many of the companies in the West are constrained by a lack of capital and/or investors seeking to cut corners and minimize burn at the expense of generating more license-able data.

For Western companies, this means facing competition not only for capital but also for licensing partners; many of whom are now turning to China for differentiated, data-rich assets.

| Chinese Licensor | Western Licensee | Area & Stage | Details |

|---|---|---|---|

| Jiangsu Hengrui Pharmaceuticals | Braveheart Bio – NewCo | Obstructive hypertrophic cardiomyopathy (cardiac myosin inhibitor) — Phase 3 China, early global rights | Upfront ~$75 MM in cash and shares + tech-transfer payment up to US$ 10 million + up to ~US$ 1 billion in milestones and royalties. Rights: exclusive global (outside Mainland China, Hong Kong, Macau, Taiwan) to HRS-1893. Source: PR Newswire |

| Jiangsu Hengrui Pharmaceuticals | GSK | COPD / respiratory + immunology/inflammation/oncology — early clinical for HRS-9821 | Upfront $500 MM; option pipeline of 11 further programs; total value up to ~$12 billion. Rights: Worldwide excluding China/HK/Macau/Taiwan. Source: GSK Press Release |

| Innovent Biologics | Roche | Small cell lung cancer and other DLL3-expressing tumors | Upfront $80 MM; up to $1 billion in milestones + tiered royalties. Exclusive global rights for IBI3009 (DLL3-targeting ADC) Source: PR Newswire |

| Hansoh Pharma | Roche | Colorectal and other solid tumors | Upfront $80 MM; up to ~$1.45 billion in milestones. Rights: exclusive global excluding Greater China. Source: Reuters |

| Argo Biopharma | Novartis | CV/Lipids siRNA | Upfront $160 MM; total deal up to US$ 5.2 billion. Rights: two early-stage cardiovascular-metabolism molecules + option rights. Source: Financial Times |

Back in the Big Apple

Finding myself back in New York (where the Guinness is plentiful), it occurred to me that we are in a phase in our industry where innovation (and the commercial underpinnings) is simply not enough anymore.

We are in the midst of an industry-wide recalibration and retrenchment, triggered in part by the influx and egress of tourist investors during COVID.

Being adaptable and flexible in an era of increasing competition and decreasing availability of risk capital is becoming increasingly critical.

Management teams (and their Boards) will have to seek earlier licenses than originally anticipated, but with less data and more competition.

CEOs committed to creating personal fiefdoms consisting of relatively large management teams and supporting personnel may have to make some tough decisions in order to cut burn and preserve capital. For some of these companies with un-license-able assets, it may be too late.

Many are operating in therapeutic areas, indications, or with modalities where early-stage licensing (let’s say, Phase I or earlier) is as common as hen’s teeth. Fewer and fewer companies will be able to navigate this complexity, perhaps resulting in more and more companies becoming extinct.

Looking ahead to 2026 (and our upcoming Year-In-Review video), we will keep an eye on a few indicators.

For example, will US VCs be able to create and raise more funds (beyond the household names)?

Will we see more AI success stories, which I am defining as more AI-discovered candidates entering Phase II clinical trials? And, if so, will that trigger an increase in the availability of investable capital?

And will we see more and more licensing of Chinese innovations? Or, will that wane as the innovation well dries?

These and other factors may drive who will or will not attend BIO-Europe 2026 in Cologne.

Post Scriptum

Thanks to all of you who stopped by the book signing, and thanks to Oliver Schnell, Andreas Macht, and the BIOCOM team for the original idea of a book signing and for supplying the space.