Will AI create more assets than pharma can absorb?

AI is often discussed as a solution to pharmaceutical research and development productivity.

It may be.

Certainly Big Pharma thinks so, given the recently announced deals with companies like Anthropic and OpenAI.

But it may also create a new kind of bottleneck.

If AI-enabled discovery platforms continue to improve, drug discovery may become less constrained by target triage, virtual screening, de novo molecule design, lead optimization, and early computational prioritization. Indeed, undruggable targets may someday be a thing of the past.

We may be entering a period in which AI-enabled discovery expands not only the speed of drug discovery, but also the range of targets, mechanisms, and molecular designs that can be explored.

That is good news.

But it also raises a harder commercial question: how will this expanding supply of early assets move through expensive development pathways in the absence of frothy public markets?

Licensing, of course.

And that is the bad news.

Why?

Because the number of licensees, and their capacity to in-license and develop very novel (higher risk) drug candidates is strategically and practically limited (and yes, we are ignoring China for a moment).

To put it another way, for a preclinical program to be licensed, there must be (at minimum) a qualified licensee with strategic interest, available budget, diligence bandwidth, and appetite for early-stage risk.

Those constraints do not automatically scale at the same rate as computational discovery throughput, even when LLMs are widely deployed to aid in due diligence and drug development.

That is where the imbalance may emerge.

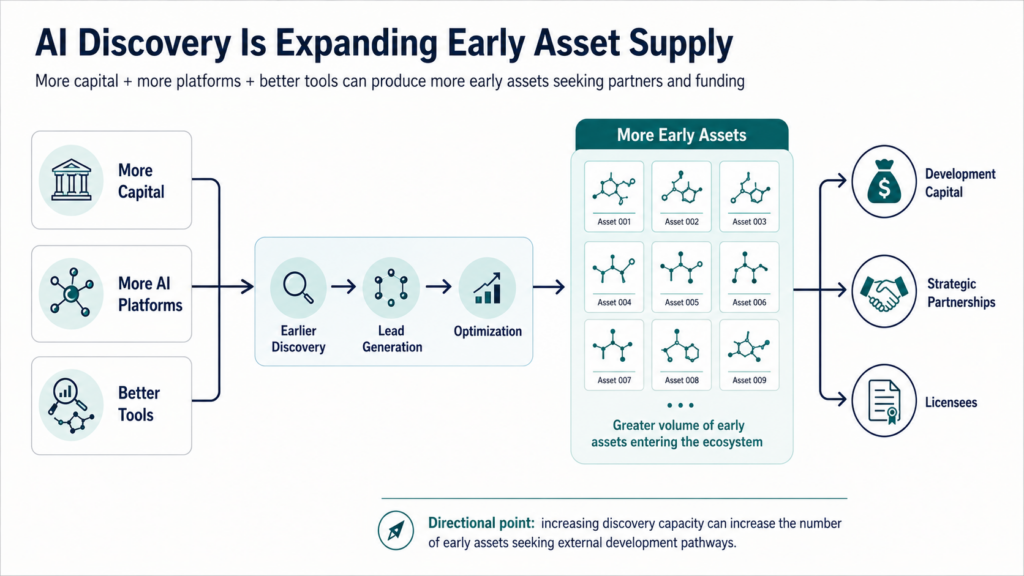

The supply side is expanding (maybe)

The clearest evidence is on the supply side of this imbalance.

The AI in drug discovery market is projected to grow from $1.86 billion in 2024 to $6.89 billion by 2029, representing a ~30% CAGR.

Major use cases include hit-to-lead identification, lead generation, and AI-enabled molecule design…precisely the tools that can increase the pace of innovative drug discovery. Identical sentiments have been expressed by BCG, SVB, and others.

These companies need adoption to justify investor expectations.

As a result, their tools will continue to be pushed into pharma, biotech, and contract development and manufacturing organization workflows.

So the results from their efforts will manifest themselves in the overall industry’s pipeline.

Now, of course, investment and market-size data are imperfect proxies.

They do not directly count licenseable preclinical candidates that emerge from AI toolkits. But they do support a basic directional point: more capital, more platforms, and better tools are being deployed toward earlier discovery, lead generation, and optimization.

All else equal, that should increase the number of early assets seeking development capital, strategic partnerships, or licensees.

AI-originated programs increasing share of industry pipeline

The second point is that AI-originated assets are no longer purely hypothetical.

Various analyses show that AI-native drug discovery companies have built expanding discovery and clinical pipelines, and that AI-originated or AI-enabled molecules are increasingly entering human testing.

This supports the directional premise that AI may increase early-asset supply, but hard numbers are tough to find.

An oft-cited 2024 analysis found that AI-discovered molecules had an 80-90% success rate in Phase I clinical trials and approximately 40% success in Phase II, with the important caveat that the Phase II sample size remains limited.

Regardless of the lack of hard data, we’ll go out on a limb here and at least speculate that the percentage of AI-discovered drug candidates in the industry pipeline is perhaps small, but growing rapidly, and will continue to grow for the foreseeable future.

The demand side looks more constrained

The demand side is harder to measure, but recent licensing data point toward selectivity rather than unlimited appetite.

For example, IQVIA reported that discovery-stage licensing deal count declined 17% from 2023 to 2024, while preclinical licensing activity fell 26% over the same period.

This matters because the AI discovery model may generate exactly the kind of early-stage assets that require licensee conviction before meaningful human efficacy data exist.

If licensees are prioritizing clinical-stage opportunities, or if internal committees are raising the bar for preclinical risk, the number of candidates will increase faster than the number of Licensees willing to act.

This does not mean large pharmaceutical companies are walking away from external innovation.

EY has estimated that roughly 45% of the pipeline assets of the top 20 pharmaceutical companies originate from external innovation through licensing, collaborations, and acquisitions.

Preclinical and Phase I candidates represent 30-50% of all Big Pharma licenses, and that has been the case for years.

The issue is not whether pharma needs external innovation. It does.

The issue is whether the capacity (even with expanding agentic AI capabilities) to evaluate, champion, fund, and develop very early assets can expand as quickly as AI-enabled discovery output.

What is also interesting about the BMS / Anthropic deal is the notion that AI will be used by BMS to “…to connect our systems and put that collective knowledge in the hands of every BMS employee to accelerate innovation for patients.”

That sounds to us like, “Let’s turn Claude loose and have it mine our data for new indications for shelved candidates, new patient subpopulations for programs dropped due to lack of efficacy, etc.”

If Claude finds these nuggets already hidden on company servers, will it result in a reduction in the number of candidates in-licensed by BMS?

Interesting question.

Deal terms may already reflect a more selective market

There are also signs that bargaining power has shifted against some early-stage companies.

More recent dealmaking data suggest that buyers are still trying to manage risk by back-ending licensing economics, even when total deal value or average upfront dollars increase.

In other words, the pressure may be less visible as a simple fall in absolute upfront payments and more visible in deal structure; manifesting itself via lower upfronts, more contingent milestones, and a stronger preference for later-stage assets.

For example, according to Blue Matter, average upfront deal value increased from 2024, but upfront payments as a percentage of total deal value declined steadily and represented only about 15% of total deal value, which they interpret as buyers mitigating risk through lower upfront payments and larger contingent payments.

BioPharma Dive, summarizing J.P. Morgan data, reported that median upfront cash and equity payments to preclinical biotechs declined from $75 million to $47 million between 2022 and the first half of 2024. Over the same period, late-stage assets obviously commanded substantially higher upfront payments.

Similarly, DealForma has reported consistent declines in Upfront payments as a fraction of Total Deal Value.

This should not be interpreted as proof that AI is causing lower preclinical deal values.

Multiple factors are involved, including capital market conditions, risk appetite, modality trends, patent cliff pressures, and therapeutic area priorities.

But the trend is directionally consistent with a market in which licensees are being more selective, pushing more value into contingent milestones, and demand stronger evidence before committing meaningful upfront capital.

The key scarcity? Not molecules. Conviction and Proof.

The emerging bottleneck may therefore be less about the ability to generate molecules and more about the ability to generate data which drives Licensee conviction.

AI can help identify targets, design molecules, optimize leads, and prioritize experiments.

It may reduce some costs and accelerate some discovery workflows.

But it does not automatically create a clear partner fit, a differentiated translational package, a credible biomarker strategy, a clean intellectual property position, a feasible development plan, or internal alignment inside a potential licensee.

In a more crowded early-asset market, and in a market where Licensees will be as busy as ever (even with agentic AI tools), the question of choosing between two licensing opportunities to enter full diligence will become even more important.

The other key scarcity: licensability analyses

I talk about licensability a lot in our courses and book. A key aspect of licensability is being able to understand potential product positioning not in today’s market, but in tomorrow’s market. Understanding how the treatment of a disease may evolve over time is critical when out-licensing because that is the strategic posture that the prospective licensee is occupying.

For example, stating that your AI-generated Preclinical drug candidate will capture 10% of the colorectal cancer TAM in 2040 is clearly insufficient. We have at least 4 subtypes of colorectal cancer, with nuanced differences in how one subtype is treated versus another. And, importantly, this will likely change over time.

With the tools and expertise at our collective disposal, there is simply no excuse for Licensors to bring superficial, generic market assumptions into increasingly sophisticated licensing discussions and expect to sign a CDA in a week.

Implications for AI drug discovery companies

That requires more than speed and lower-cost.

It requires differentiated biology, human-relevant translational evidence, a defensible intellectual property plan, a sensible clinical development path (even though the Licensee may disagree), and a clear positioning hypothesis relative to evolving treatment paradigms.

For companies built around AI-enabled discovery, business development strategy should therefore begin much much earlier.

Partner mapping, competitive positioning work, evidence-gap analysis, and licenseability assessment should not wait until a candidate has already been selected.

They should be part of the discovery strategy itself. It may be even better to say that they should be part of the company formation plans long before that first pitch deck or business plan is created.

Conclusion

The data do not yet prove that an AI-driven preclinical licensing bottleneck is inevitable.

Perhaps the more defensible conclusion is that the conditions for such a bottleneck are becoming visible.

The supply side is unquestionably expanding. More AI-originated programs are entering IND-enabling studies and the clinic.

But early-stage licensing appears increasingly selective, and further hampered by both bandwidth and development capacity. Whether or not AI can relieve these pressures remains an open question.

The next bottleneck in drug development may not be finding another molecule.

It may be convincing the right partner that this molecule deserves to move ahead.